Health care costs are one of the biggest expenses in retirement, after housing and transportation costs. As the health care cost inflation continues to outpace standard inflation, health care costs are expected to account for a larger portion of the retirement budget.

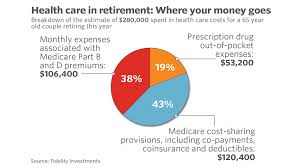

A couple that retired in 2019 required $285,000 (after tax) in current dollars to meet medical expenses during retirement, as per Fidelity Investments. This estimate excludes long-term care expenses. A single woman retiree is estimated to require $150,000 in today’s dollars while a single man requires $135,000. Though this amount of $285,000 has marginally increased from the value of $280,000 in 2018, the rise has been significant when compared with 2015, when the value was $245,000.

Over the 4-year period of 2015 – 2019, health care costs have increased by 16.3%. This increase is not just due to inflation, but the cost of services and treatment has also been increasing. As innovations take place in the health care industry, the costs also rise more than the standard inflationary rates.

Here is another interesting fact – if you feel that you are healthy, your health care costs would be lower. The fact is NO! If you are healthy, your life expectancy would be higher. So even if your annual costs are lower, the total payments over your lifetime would be higher.

As per HealthView Services, a healthy 55-year old woman is expected to spend an average of $13,165 in medical costs annually at 65. Another woman of the same age, suffering from Type – 2 diabetes, is expected to spend $16,635 annually towards health care costs. The annual payout is obviously more for the Type 2 diabetic woman due to relatively poor health.

Over their lifetime, the healthy retiree is expected to pay $424,875 towards medical expenses, as per HealthView Services. The diabetic retiree would have lower life expectancy and is expected to spend $266,163 only during retirement. The healthy retiree has lower annual payout, but due to their longer life, they will have additional years of expenses. This causes the overall expenses to be much higher for the healthy retiree than their diabetic counterpart.

Financial planning for retirement is very important, especially to meet the unpredictable health care costs. Merely having Medicare coverage is not enough, since it does not cover several costs. A major cost element, not covered by Medicare, is the cost of assisted living. As per Genworth Financial, the national median cost of assisted living was $48,000 in 2018 and this cost has been rising. Dental costs are also not covered by some Medicare plans and can add significantly to retirement health care costs.

Given the sizable amount of aggregate health care costs in retirement, it is prudent that you start planning now. You can take steps such as funding your Health Savings Account (HSA) to ensure that you have enough coverage to fund your expenses in retirement. Align your financial portfolios with your retirement objectives to have synchronized cash inflows and outflows when you retire.

Part of our services as a Certified Financial Planner is to plug these costs into all financial plans to make certain our clients are not hit with unexpected costs during their retirement that they haven’t considered as part of their overall financial forecasts.