As investors, we want to have minimum risk and, while doing so, maximize our returns. Dollar-Cost Averaging (DCA) is an investing strategy that many investing gurus will suggest for new investors. In this article, we will dive into what DCA is and if it makes sense or is just another marketing gimmick.

Dollar-Cost Averaging (Dollar Cost Averaging) is a risk management approach to buying assets where a large investment is divided into smaller, usually equal-sized investments to be made regularly over a specified period.

- You have $1000 to invest in XYZ. You divide your investment into ten $100 purchases(no matter the stock price) that you will make every 2-week pay period for 20 weeks.

Your buying price will be an average of 20 weeks. This way, you are not “timing the market” with DCA, taking emotion out of your purchases which is always good. DCAs other benefits are that it helps to build a habit of investing, and it lowers risk by avoiding lousy timing. It is nearly impossible to determine a bottom of a price decline.

These are great attributes to have, but DCA may be a bit too simplistic for the seasoned investor.

The first issue is that a market rises over time and at a reasonably predictable rate(S&P is roughly 8%/yr). Therefore in the above example, your first $100 investment will be making that predictable rate for 18 weeks longer than the last. Over two-thirds of the time, a lump sum has been shown, on average, to perform better than DCA because of this.

Second, if you are identifying suitable investments, then you have determined that they are already at a low price. Investing does involve research, and if you are taking a more passive approach, a bad pick is a bad pick, and you are just throwing money away consistently with DCA rather than in a lump sum.

DCA’s passive approach can take thinking out of investing. When investing with DCA, one can keep doing the same thing, not following the market. What if, after the first $100, the company puts out a worrying statement? Should you continue to invest? Or likewise, they release good news, will you miss a short-term gain by not increasing your company exposure?

With DCA, fees can add up; if you are charged a standard trade fee, you will multiply this for all of your purchases using DCA, or if the prices are a more significant percentage, the smaller the size.

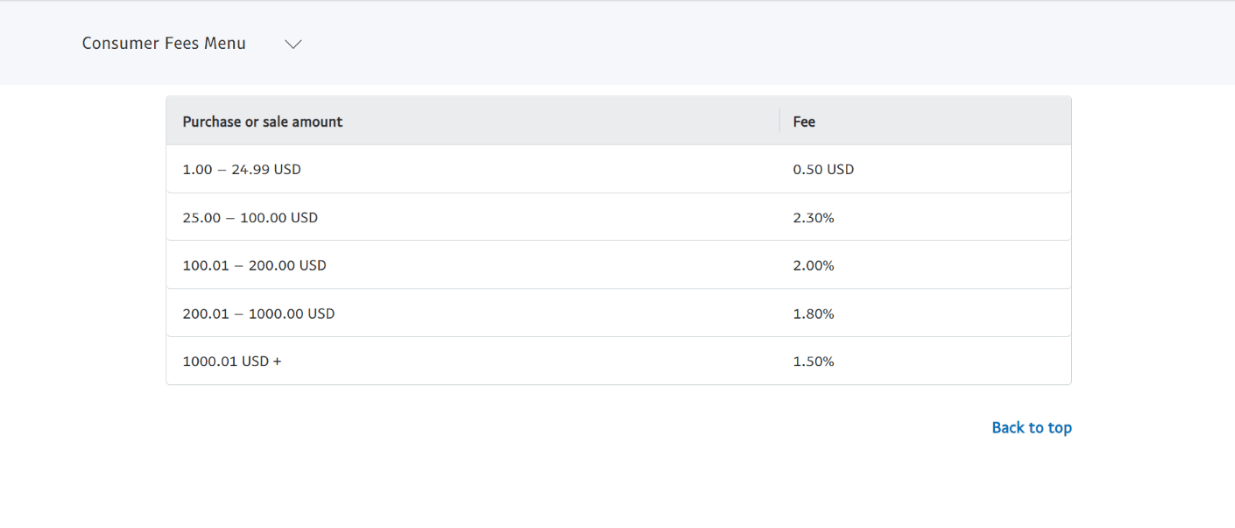

Paypal’s crypto fees

Our $1000 example buying from PayPal would either cost $23 or $18. This $5 means lower returns that add up.

- Pro tip: Always know your fees; just a $0.01 change buying $100.01 or $1000.01 would make a $3 difference as well.

DCA lowers some risks but not all. For example, DCA can help you time the bottom in a bear market, but should you be investing in a bear market? Imagine you start a DCA cycle in September 2000 or October 2007?

You would have years of declines that would then take years to come back as well. During these Bear periods, there were plenty of indicators that the economy was terrible and would not turn around for a while.

You would have years of declines that would then take years to come back as well. During these Bear periods, there were plenty of indicators that the economy was terrible and would not turn around for a while.

Summary

For a less experienced investor or one who needs to create an investing habit, DCA can be a great tool to average out market swings. On the other hand, DCA can lower overall returns for the more experienced investor with an investment plan. Either method will eventually get you to your investment goals, and that is what we are looking for.

Remember, never put at risk more than you can afford to lose, and we wish you good luck with all your trades.

If you’re pondering this situation, whether to invest all at once or use dollar-cost averaging, please feel free to reach out to me at Chase Thomas by email at cthomas@alphawealthfunds.com and I’ll be happy to discuss it and possibly show you even better strategies to accomplish your goals.